Canadians often walk into vehicle financing focused on one number: the monthly payment. That number matters, but it can hide the real cost of borrowing, the speed of depreciation, the risk of negative equity, and the impact of add-ons that quietly become part of the loan. With vehicle prices, insurance costs, interest rates, and used-car values all shifting, financing decisions now require more scrutiny than they did a few years ago. These 18 mistakes show where buyers commonly lose leverage, stretch budgets too thin, or sign contracts without fully understanding the long-term cost.

Focusing Only on the Monthly Payment

A low monthly payment can feel like a victory at the dealership desk, especially when the salesperson presents it as the difference between “affordable” and “too expensive.” The problem is that monthly payments can be lowered by stretching the loan term, increasing the down payment, rolling in trade-in debt, or adjusting the financing structure. None of those moves automatically makes the vehicle cheaper.

A shopper who compares $650 per month with $575 per month may miss the bigger picture: the lower payment could cost thousands more over the full term. Canadian consumer guidance repeatedly warns buyers to look at the total cost of borrowing, not just the payment amount. The practical mistake is emotional. Once a payment “fits,” many buyers stop negotiating the vehicle price, interest rate, fees, and add-ons.

Accepting an Overly Long Loan Term

Longer auto loans have become tempting because they make expensive vehicles look manageable. A seven- or eight-year loan can turn a painful monthly payment into something that seems easier to handle. But the trade-off is time: more months of interest, a longer period before equity builds, and a higher chance the vehicle will need repairs while payments are still ongoing.

This matters in Canada because vehicles depreciate while loan balances decline slowly, especially early in the repayment schedule. A family financing a crossover for 84 months may still owe a large balance when the warranty is gone, tires need replacing, and insurance premiums have risen. The loan may feel reasonable in year one but restrictive in year five. Shorter terms are harder on cash flow, yet they reduce the risk of being trapped.

Not Comparing Financing Offers Before Visiting the Dealer

Many buyers treat dealership financing as the default because it is convenient. The vehicle, trade-in, loan approval, and paperwork all happen in one place, often within a few hours. Convenience, however, can blur the difference between a competitive financing offer and one that simply feels easy to accept.

Pre-checking options through a bank, credit union, or online lender gives shoppers a benchmark before negotiating. Without that benchmark, it becomes harder to know whether the dealer-arranged rate is strong, average, or expensive. Even a small rate difference can matter on a five-figure loan. For example, a buyer financing $42,000 over several years may focus on whether the payment feels acceptable, while a slightly lower interest rate could save enough to cover winter tires, insurance increases, or several months of fuel.

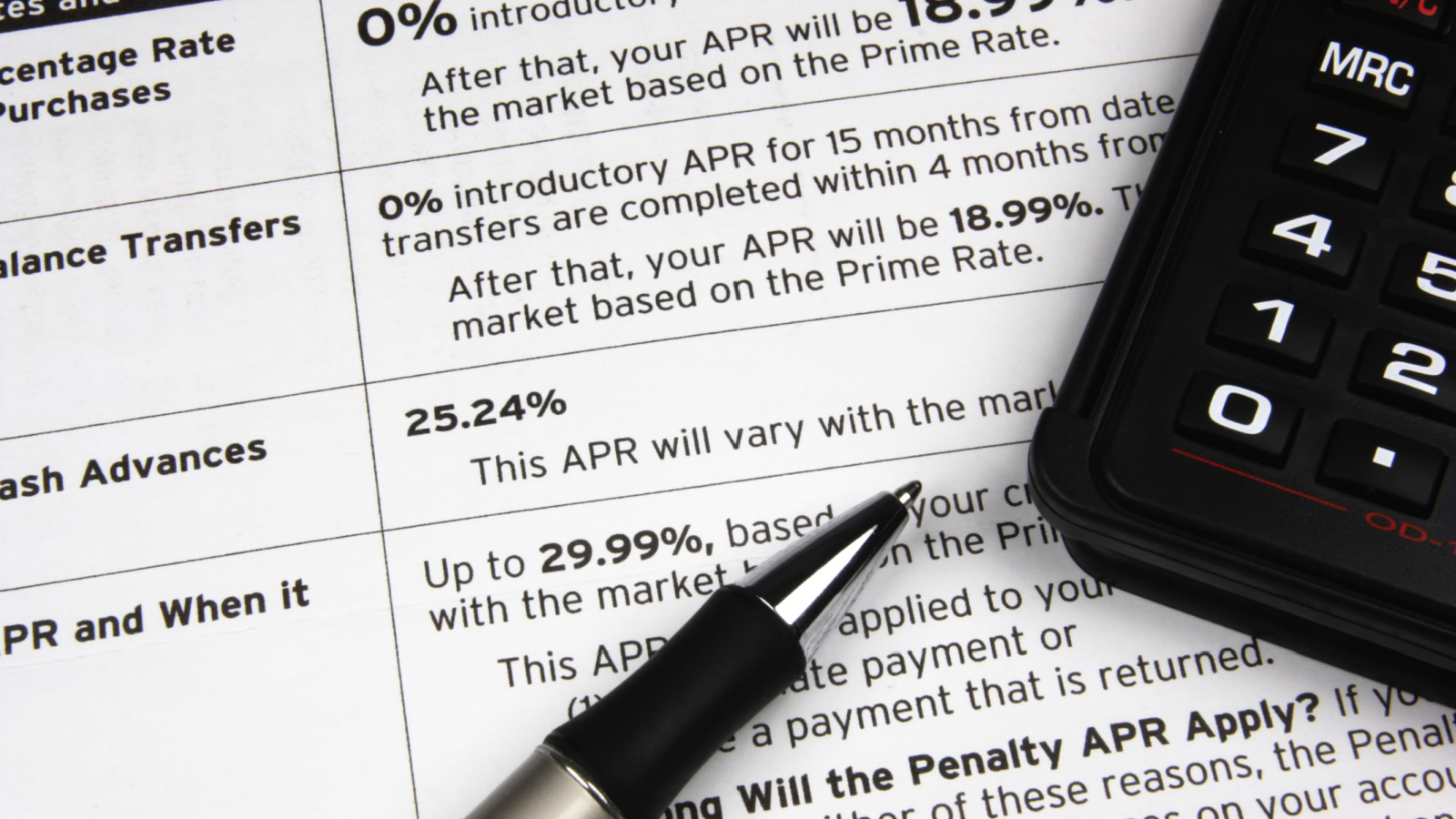

Ignoring the Total Cost of Borrowing

The sticker price is not the final cost, and the monthly payment is not the full story. Interest, taxes, fees, warranty products, insurance products, and loan length all shape the amount paid by the end. A vehicle listed at one price can become dramatically more expensive once everything is financed together.

This mistake often appears when buyers do not ask for a full cost breakdown before signing. A contract may show the amount financed, annual percentage rate, term, total interest, and total obligation, but those numbers are easy to skim when the delivery date is close. A careful buyer pauses on the total repayment figure. That is the real price of choosing the loan. In many cases, the final number feels very different from the advertised price that first attracted attention.

Rolling Negative Equity Into the Next Loan

Negative equity means the borrower owes more on the current vehicle than the vehicle is worth. It can happen after a small down payment, a long loan term, fast depreciation, or an early trade-in. The costly mistake is rolling that unpaid balance into the next vehicle loan and treating it like it disappeared.

It has not disappeared. It has been moved. A Canadian driver trading in a vehicle with $6,000 of negative equity may end up financing that old debt on top of the next purchase. That increases the new loan balance, raises the risk of being underwater again, and may make the next trade-in even harder. Negative equity can become a cycle: one expensive decision quietly follows the buyer into the next vehicle, then the next.

Skipping a Meaningful Down Payment

A down payment does not just reduce the amount borrowed. It also creates a buffer against depreciation. Vehicles usually lose value as they age and accumulate kilometres, and a buyer who finances nearly the entire purchase price starts with less protection if market values fall.

Small or zero-down offers can be attractive, especially when household budgets are tight. But they often leave the borrower exposed. Imagine financing almost the full price of a new SUV, then trying to sell it two years later because family needs changed or insurance became too expensive. If the loan balance remains above the vehicle’s market value, the owner must cover the gap. A down payment is not glamorous, but it can prevent an ordinary life change from becoming a financing problem.

Treating the Interest Rate as Non-Negotiable

Some buyers assume the posted or offered finance rate is fixed. In reality, financing terms can vary by lender, credit profile, promotion, vehicle type, loan term, and dealer arrangement. Even when a buyer cannot qualify for the lowest advertised rate, there may still be room to compare offers or adjust the structure.

The mistake is accepting the first number without asking what it is based on. A buyer with strong credit may qualify for better terms than initially shown. Another may be better served by a smaller loan, larger down payment, or shorter term. The rate should be treated like part of the purchase, not an afterthought. A half-point or full-point difference may look minor on paper, but over years it can become a real household expense.

Financing Add-Ons Without Questioning Them

Extended warranties, rust protection, tire-and-rim coverage, protection packages, insurance products, and service plans can all sound reasonable when presented beside a major purchase. The payment difference may look small because the cost is spread over the loan. That is exactly why buyers need to slow down.

A $2,000 add-on does not feel like $2,000 when it adds only a few dollars per payment, but financing it means interest may also be paid on that product. Some add-ons are useful for certain drivers, especially those keeping a vehicle long term or driving in harsh conditions. Others duplicate existing coverage or offer limited value. The mistake is not buying any protection; it is accepting bundled products without asking what they cost, whether they are optional, and how claims actually work.

Forgetting That Taxes and Fees May Be Financed Too

In Canada, buyers often focus on the negotiated vehicle price, then feel surprised when the financed amount is much higher. Taxes, licensing, registration, dealer fees, freight, pre-delivery inspection, and optional products can all change the final number. If rolled into the loan, they become part of the amount that generates interest.

This mistake is common because the worksheet can be more complicated than the conversation. A buyer may remember agreeing to a vehicle price but not fully absorb the “amount financed” line. In provinces with all-in price advertising rules, certain mandatory dealer charges must be included in advertised prices, but taxes and licensing can still sit outside the headline number. The safest habit is to ask for an itemized purchase agreement and compare it against the advertised price before discussing payments.

Not Understanding All-In Price Rules

All-in pricing rules are meant to protect buyers from advertised prices that grow once they arrive at the dealership. In Ontario, for example, dealer advertisements generally must include the fees and charges the dealer intends to collect, except HST and licensing. Across Canada, drip pricing has also drawn attention because it can make the first price shown less meaningful than the final price paid.

The mistake is assuming every added fee is automatically legitimate or unavoidable. A buyer may see an administration fee, certification fee, preparation charge, or other line item and accept it because it appears official. Some fees may be allowed, but the key question is whether they were properly disclosed and whether the advertised price was attainable. Financing magnifies the issue because extra charges do not just raise the purchase price; they can increase interest paid over time.

Underestimating Depreciation

Depreciation is easy to ignore because it does not arrive as a monthly bill. The vehicle simply becomes worth less over time. But depreciation matters enormously in financing because the loan balance and market value move in opposite directions: one slowly declines, while the other may fall quickly.

Canadian used-vehicle values have been through unusual swings, and retained value differs widely by brand, segment, mileage, condition, and fuel type. A buyer who chooses a vehicle mainly because the payment fits may later discover it is worth much less than expected. That becomes a problem when selling, trading, refinancing, or dealing with a total-loss insurance claim. The smart move is to research resale values before buying, not after the financing contract is already signed.

Trading In Too Early

Early trade-ins can be expensive when the loan has not had enough time to catch up with depreciation. Drivers sometimes trade because they want newer safety features, lower fuel costs, more space, or relief from repair worries. Those reasons may be valid, but the financing math can still be punishing.

The mistake is asking only, “What will my new payment be?” instead of, “What happens to my current loan balance?” If the trade-in value is lower than the payoff amount, the shortfall must be paid or financed. A buyer may leave with a newer vehicle but also with old debt hidden inside the new contract. Waiting longer, making extra principal payments, or selling privately can sometimes reduce the damage. The timing of a trade-in can be just as important as the trade-in value.

Assuming 0% Financing Is Always the Best Deal

Zero-percent financing sounds unbeatable, and sometimes it is. But buyers still need to compare the entire transaction. A low-rate or zero-rate offer may be tied to a specific term, model, price, or loss of a cash rebate. The best financing rate does not always equal the lowest total cost.

For example, one buyer may be offered 0% financing at full price, while another may receive a manufacturer rebate with a higher rate. The better choice depends on the amount financed, term length, down payment, and whether the buyer can repay early. The mistake is treating the rate as the only number that matters. A vehicle deal has several moving parts, and the most attractive headline can distract from a weaker selling price or less flexible contract.

Not Reading Prepayment Terms

Some buyers plan to finance the vehicle, then pay it down faster when cash flow improves. That can be a smart strategy, but only if the loan allows it without penalties or awkward restrictions. Not all financing arrangements feel the same once extra payments enter the picture.

The mistake is assuming every auto loan is fully flexible. A buyer may intend to use a work bonus, tax refund, or sale of another asset to reduce the balance, then later discover limitations or unclear procedures. Even when prepayment is allowed, the borrower should know whether extra money goes directly to principal and how to make that instruction clear. Reading the prepayment section before signing can preserve options. Flexibility has real value when income, rates, or household priorities change.

Ignoring Insurance Costs Until After Approval

A vehicle can fit the financing budget and still be unaffordable once insurance is included. Premiums vary based on driver profile, location, claims history, vehicle type, repair costs, theft risk, and coverage choices. In some Canadian cities, the insurance quote can change the entire affordability calculation.

This mistake often happens when buyers fall in love with a specific trim, engine, or model before getting a quote. A vehicle with advanced sensors, high theft rates, expensive body panels, or performance-oriented parts may cost more to insure than expected. The loan approval only confirms the lender is willing to finance the purchase; it does not confirm the household can comfortably carry every ownership cost. Getting insurance estimates before signing can prevent a payment that looks manageable from becoming stressful.

Forgetting Maintenance and Repair Timing

Financing decisions often assume the vehicle will remain predictable throughout the loan. That assumption weakens as the term grows longer. Tires, brakes, batteries, fluids, suspension components, and out-of-warranty repairs can arrive while payments are still due. For used vehicles, those costs may arrive sooner.

The mistake is budgeting for the loan as if it is the only major vehicle expense. A driver with a six- or seven-year term may eventually face monthly payments and repair bills at the same time. This can be especially frustrating when a vehicle was chosen to “save money” compared with a newer or more reliable option. A realistic financing decision includes a repair reserve. If there is no room for maintenance, the payment may already be too high.

Skipping the Vehicle History and Lien Check

Used-vehicle financing adds another layer of risk. A clean-looking car can have accident history, inconsistent service records, odometer concerns, registration issues, or an existing lien. Financing a vehicle without checking its history can leave the buyer paying for problems that were already present.

A lien check matters because a previous lender may still have a financial interest in the vehicle. Vehicle history reports are not perfect, but they can reveal important clues, including accident records, title branding, service patterns, and valuation context. The mistake is assuming financing approval means the vehicle itself is a safe purchase. Lenders assess credit and collateral, but buyers still need to verify what they are buying. A pre-purchase inspection and history report can protect both the wallet and the loan.

Letting the Dealership Bundle the Trade-In, Price, and Financing Together

Dealership negotiations often combine several decisions: purchase price, trade-in value, loan rate, term, add-ons, and monthly payment. Bundling everything can make the deal feel smooth, but it also makes it harder to see where money is being gained or lost.

The mistake is negotiating only the final payment. A dealer may increase the trade-in allowance while holding firm on the vehicle price, or lower the payment by extending the term. Another deal may look generous because of a rebate, while the financing rate offsets the benefit. Separating each part creates clarity: first the vehicle price, then the trade-in value, then the financing, then optional products. When each number stands on its own, weak spots become easier to challenge.

22 Things Canadians Do to Their Cars in Spring That Mechanics Hate

Spring brings relief to many Canadian drivers after months of snow, freezing temperatures, and icy roads that put serious strain on vehicles. As temperatures rise across the country, drivers begin washing cars, switching tires, and preparing vehicles for warmer weather and upcoming road trips. However, mechanics across Canada notice the same mistakes every spring when drivers attempt to recover from winter damage. Road salt, potholes, and harsh winter driving conditions often leave vehicles with hidden problems that drivers ignore. Some spring habits even create new mechanical issues that could have been avoided with proper maintenance. Here are 22 things Canadians do to their cars in spring that mechanics hate.

{kind=link}