Car shopping in Canada increasingly wears people down not because the choice is exciting, but because the process often feels designed to blur the real deal until the very end. Consumer regulators, financial watchdogs, and recent market research all point to the same pressure points: hidden costs, financing complexity, disclosure gaps, and a sales environment that can reward confusion more than clarity.

These 18 tactics capture the patterns that shoppers, complaint handlers, and industry observers keep circling back to. Some are obvious the moment a quote changes. Others only become clear after a contract is signed, a trade-in is rolled over, or a warranty turns out to cover far less than expected. Together, they help explain why buying a vehicle can feel less like a straightforward purchase and more like an endurance test.

An Attractive Price That Somehow Never Exists in Real Life

One of the fastest ways to exhaust a shopper is to start with a number that looks compelling online, then slowly reveal that it was never the real number at all. Across Canada, regulators have spent years warning dealers about “drip pricing,” the practice of advertising a price that becomes unattainable once mandatory charges appear later. For shoppers, the damage is not just financial. It wastes time, distorts comparisons, and creates the sense that every promising lead may be built on a technicality. A search that should narrow choices turns into a detective exercise, with buyers trying to decode what a posted price actually includes.

That frustration deepens because the entire point of an advertised price is supposed to be easy comparison. When the advertised figure excludes charges the dealer already intends to collect, the shopper is no longer comparing vehicles on equal terms. In Ontario and Alberta, all-in pricing rules exist precisely because hidden mandatory charges undermine honest shopping. Yet the tactic persists in subtler forms, often through disclaimers, delayed explanations, or selective itemization that changes the emotional feel of the deal even when the final paperwork eventually catches up.

Fees That Reappear Under New Names

A dealer does not always need a dramatic bait-and-switch to make a transaction feel draining. Sometimes all it takes is an alphabet soup of line items: admin fee, documentation fee, inspection fee, protection fee, levy recovery, preparation fee. A shopper may understand the vehicle price, then get buried under labels that sound official enough to discourage pushback. The practical result is confusion over which charges are required, which are negotiable, and which should already have been included in the advertised amount. The more unfamiliar the language, the easier it becomes for buyers to doubt their own instincts.

This matters because fee design can shape behaviour even before it changes the total. A consumer who feels uncertain about whether a charge is legitimate is already at a disadvantage. Alberta’s regulator explicitly warns that businesses must not mislead customers into believing a fee is mandatory or required by law when it is not. Ontario’s rules similarly require intended fees to be included in advertised pricing, with only narrow exceptions such as HST and licensing. When line items multiply after the emotional commitment to a vehicle has already formed, resistance gets harder, and exhaustion becomes part of the sales strategy whether anyone admits it or not.

“It’s Already Installed” as a Way to Make Add-Ons Feel Non-Negotiable

A familiar dealership move is to treat optional extras as settled facts. Nitrogen-filled tires, wheel locks, anti-theft etching, paint protection, or security packages are presented as though they are inseparable from the vehicle because the work has already been done. For the shopper, this transforms a choice into an awkward confrontation. Declining no longer sounds like a simple budget decision; it sounds like refusing something that has allegedly become part of the inventory. That framing can make people feel unreasonable for objecting, especially after investing time in a test drive, credit discussion, and trade-in conversation.

Canadian regulators have flagged this issue directly. Ontario’s all-in advertising guidance says pre-installed products and services, including etching, warranties, security products, and similar extras, must be reflected properly in the advertised price if the dealer intends to charge for them. Alberta’s rules are even more explicit in listing add-ons such as paint protection and etching among charges that cannot be disguised or misrepresented. The tactic is exhausting because it collapses the difference between optional and unavoidable. By the time the buyer is told something “comes with the car,” the real negotiation has already been narrowed, often without the shopper realizing when that happened.

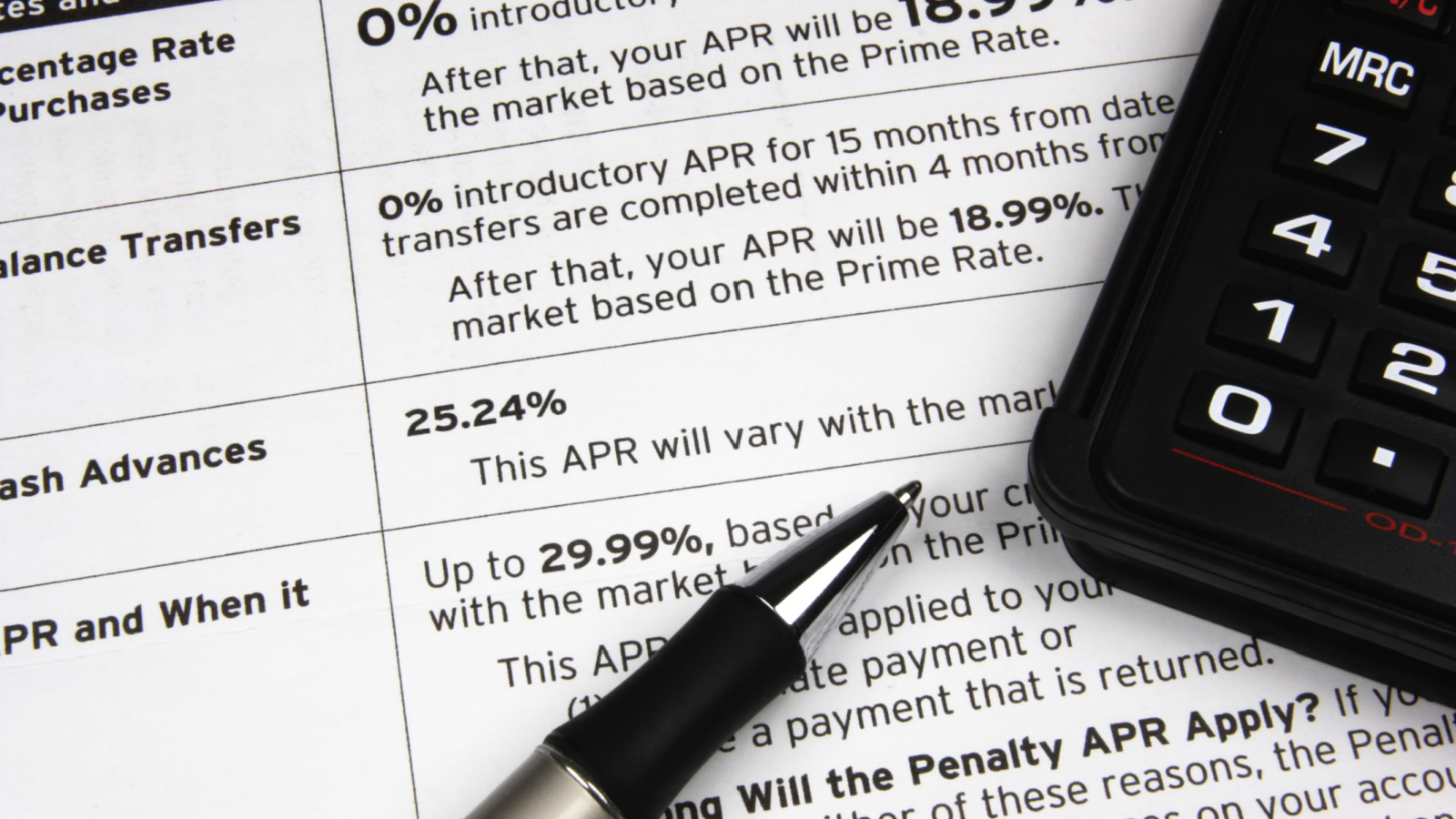

Steering the Conversation to Monthly Payment Instead of Total Cost

Many buyers arrive focused on affordability, and dealers know it. That is why the conversation often shifts away from the full transaction price and toward a single monthly number as early as possible. Once that happens, the discussion becomes easier to manipulate. A payment can be lowered in many ways without making the deal better: lengthening the term, adjusting the down payment, bundling add-ons into financing, or burying earlier negative equity. The shopper hears a manageable figure and feels relief, while the total cost quietly grows behind the curtain. It is a classic sales reframing technique because it aligns with what stressed buyers most want to hear.

Canadian financial guidance repeatedly warns against this trap. The Financial Consumer Agency of Canada tells borrowers to compare not just interest rate but financing fees, payment schedule, total amount financed, and overall term. Its examples show how dramatically a lower-looking payment can conceal a higher final cost. This tactic is mentally tiring because it forces buyers to fight the format of the conversation itself. Instead of assessing a vehicle on straightforward numbers, they must keep dragging the discussion back to total price, borrowing cost, and contract length. That extra vigilance turns what should be a major purchase into a constant act of translation.

Stretching the Loan Until the Vehicle Outlives the Excitement

Long loan terms are often sold as the answer to immediate budget pressure. In the showroom, a 72-, 84-, or even 96-month term can make an expensive vehicle feel attainable because the monthly payment shrinks to a psychologically tolerable number. What gets lost is that the buyer is not escaping cost. The debt is simply being spread across more years, generating more interest and keeping the owner tied to the vehicle long after the novelty has faded. That becomes especially punishing when repair bills rise during the same period the borrower is still making payments on an aging asset.

Federal guidance has been unusually clear on this point. FCAC’s sample comparison shows that a $25,000 vehicle financed at 5% costs far more over 84 months than over 36 months, even though the longer term looks easier month to month. OMVIC likewise warns that extended terms increase the chance of negative equity because the principal is repaid slowly while the vehicle depreciates. The tactic is exhausting because it appeals to present-tense survival while quietly worsening the long-term picture. Buyers leave thinking the dealer solved an affordability problem, when in many cases the problem has simply been stretched over years.

Rolling Old Debt Into the Next Deal and Calling It Progress

Trade-ins can feel like fresh starts, but they are often used to hide unfinished business. When a shopper owes more on the current vehicle than it is worth, the shortfall does not disappear. It gets added to the next loan. In practice, that means a person may think they are financing one car while still paying for part of the last one. Dealers and finance staff sometimes present this in smooth, solution-oriented language: “We can absorb the difference,” or “We can work the balance into the new payment.” The language sounds helpful because it removes immediate friction. The math is far less forgiving.

Canadian regulators have been warning about this cycle for years. OMVIC’s examples show how a buyer with an eight-year loan can end up carrying thousands in negative equity into the next purchase, borrowing far above the replacement vehicle’s price. The short-term convenience is what makes the tactic potent. Instead of forcing a painful reckoning, it converts an existing problem into a larger, more opaque future obligation. For shoppers, that is exhausting because the transaction feels cleaner than it is. The dealer offers motion, not resolution, and the buyer leaves with a newer vehicle but often a worse debt position than before.

Trade-In Numbers That Stay Fuzzy Until the Deal Is Almost Done

Another draining tactic is to blur the boundaries between three separate negotiations: the price of the new vehicle, the value of the trade-in, and the financing terms. When those numbers stay bundled together, shoppers struggle to tell where they are gaining and where they are losing. A dealer may appear generous on the trade while holding firm on the vehicle price, or vice versa, leaving the impression of progress without real clarity. Because people often judge the transaction by emotional markers rather than a clean worksheet, a “good trade number” can mask a weak overall deal.

That is why disclosure rules matter. Alberta requires trade-in information and, where applicable, the remaining loan balance to be clearly incorporated into the bill of sale. In Ontario, OMVIC directs consumers toward tools such as Canadian Black Book and vehicle history resources precisely because uninformed trade-ins are easy places to lose money. The tactic is tiring because it creates mental overload. A shopper has to evaluate not one transaction but several interlocking ones at once, often while sales staff move quickly between them. When the numbers are not isolated, even careful buyers can walk away feeling they won on one front while quietly giving ground on two others.

Conditional Approval That Feels Final Until It Suddenly Is Not

Few experiences sour a purchase faster than being told the deal is done, only to hear later that financing “fell through” and new terms are needed. This is the logic behind spot-delivery or yo-yo-style financing, where a buyer takes possession before the financing is truly final or before the conditions are fully understood. The dealership gets the emotional advantage of commitment: once the customer has driven the vehicle home, arranged insurance, shown family members, or mentally moved on from the old car, the pressure to preserve the deal rises sharply. Returning to renegotiate no longer feels neutral. It feels like a reversal.

Canadian buyers are not imagining the risk. Consumer-facing guides in the Canadian market describe the pattern clearly, and federal tax interpretations also reflect the existence of conditional sales structures later assigned to financial institutions. The tactic is exhausting because it weaponizes momentum. What should be the last step in the process becomes a new round of vulnerability, often with worse terms, a larger down payment, or urgency to re-sign. Even when the original paperwork technically allowed for conditions, the lived experience for many buyers is that finality was implied long before it truly existed, and that mismatch is what makes the experience so punishing.

Deposit Pressure Before the Shopper Is Ready

A deposit can look harmless, even practical. It is often framed as a way to “hold the vehicle,” “show seriousness,” or “get the paperwork started.” But once money changes hands, the psychology of the deal changes with it. Buyers who were still comparing options may start feeling locked in, especially if they are unsure whether the deposit is refundable. That uncertainty becomes more powerful in a market where shoppers fear losing a vehicle they like. The tactic is not always illegal or improper, but it is undeniably effective at converting interest into commitment earlier than many buyers intend.

Ontario guidance makes the stakes plain. If no contract has been signed, a deposit must be returned on request; after signing, there is generally no cooling-off period, and a dealer may keep some or all of the deposit as liquidated damages if it agrees to unwind the contract. That sharp legal shift is why deposit pressure feels so exhausting. A seemingly small gesture can turn into a threshold moment with real consequences. Buyers who think they are only reserving time to decide may discover that the dealership treated the deposit as the start of a far more binding process than the conversation suggested.

Credit Applications That Move Faster Than Consent

Financing conversations can become uncomfortable when a shopper realizes the deal is advancing further than expected. Someone may think they are discussing scenarios or requesting a quote, only to later find credit checks have already been run. Canada’s privacy regulator has investigated precisely this kind of dealership conduct, including a case in which a buyer discovered multiple credit checks while negotiations were still unresolved. Even when the financial impact is limited, the emotional impact is significant. It signals that the transaction may already be moving inside systems the customer has not fully agreed to enter, which immediately changes the trust level.

This tactic becomes especially tiring because financing is complicated enough without uncertainty over what stage the process is actually in. FCAC advises consumers to sign an application if they want an approval and quote, but not to sign a sales agreement until they are ready to make a final decision. That separation matters. When shoppers lose track of whether they are exploring, applying, or committing, dealership control increases. The process stops feeling transparent and starts feeling slippery. For consumers already juggling price, insurance, and trade-in decisions, unclear consent around credit activity adds one more layer of stress to a purchase that is already demanding.

The Finance Office as a Second Negotiation

Many buyers think the hard part ends once they agree on the vehicle, but the finance office often becomes a second sales floor. By that stage, decision fatigue is high, the paperwork stack is growing, and the customer wants to be done. That is exactly when add-on products become easiest to sell: extended warranties, tire-and-rim protection, key replacement, theft products, paint packages, debt protection, and other extras presented in a rapid sequence. Each item can be framed as prudent, affordable, or small when rolled into the monthly payment. The cumulative effect, however, can materially change the cost of the purchase.

Canadian regulators do not forbid these products outright, but they do insist on proper disclosure and compliance. AMVIC notes that extra fees should be disclosed during negotiation, not after the purchase price has already been established. OMVIC’s guidance on extended warranties emphasizes that these products vary widely and may be marked up, negotiated, or backed by third parties rather than the manufacturer. What makes the finance-office tactic exhausting is timing. It appears after the buyer has already spent hours reaching what felt like a conclusion. Instead of closure, the shopper faces another high-pressure round, this time with more fatigue and less bargaining energy.

Warranties Sold on Reassurance, Not on What They Actually Cover

Extended warranties are appealing because they speak directly to fear. Cars are expensive, repairs can be unpredictable, and buyers understandably want protection. The problem is that the word “warranty” can do emotional work far beyond the contract itself. Many shoppers assume broad coverage when the reality may include deductibles, claim limits, exclusions, waiting periods, repair-facility restrictions, kilometre caps, or overlapping coverage with an existing manufacturer warranty. The dealer’s pitch often leans on peace of mind; the product’s fine print may deliver something much narrower. That mismatch leaves buyers feeling less protected than promised and more irritated for having paid extra to discover it.

OMVIC’s consumer guidance makes this issue unusually concrete. It tells buyers not to assume the warranty offered by a dealer is from the manufacturer, warns that coverage varies widely, notes that dealers usually mark up extended warranties, and points to claim limits, deductibles, exclusions, and activation fees as issues worth understanding before purchase. In other words, the details matter more than the label. The tactic is exhausting because it takes advantage of a moment when shoppers are already mentally spent and most susceptible to buying reassurance as a feeling instead of coverage as a contract.

Telling Buyers There Is No Choice but Financing

A particularly frustrating modern variation is the “finance-only” sale, where the dealership treats in-house financing as the required path to the vehicle. For a consumer who arrives pre-approved, wants to pay cash, or simply prefers a different lender, this can feel less like a transaction and more like a gatekeeping exercise. The dealership may not always frame it aggressively; sometimes it is presented as store policy, the route to a lower sticker price, or the only way to access a certain unit. Even when lawful as a business policy, it adds another layer of exhaustion because the buyer is no longer comparing just vehicles but also the acceptable methods of paying for them.

AMVIC has addressed this directly, noting that it gets complaints and questions about finance-only options. The regulator says businesses can choose how they accept payment, but consumers should not be told such arrangements are regulator-endorsed, and they should not be told they must keep a loan for six months. Under Alberta law, non-mortgage loans can generally be paid off early without penalty. This tactic wears people down because it blurs store policy, financing advice, and legal rights. A shopper who thought the deal was about a car suddenly has to navigate a dealership’s preferred profit structure as well.

Fine Print and Finality Arriving After the Emotional Decision

For many consumers, the emotional decision to buy happens before the legal decision is fully understood. That gap is where exhaustion thrives. After a test drive, a trade discussion, a financing conversation, and hours at the store, the buyer is often ready for relief. The contract becomes the last obstacle rather than the central document. Dealers do not need to hide anything spectacular; they only need the customer to sign before fully absorbing the implications. In Ontario, that matters enormously because there is generally no cooling-off period once the agreement is signed. “I changed my mind” is not a reset button in this market.

OMVIC’s contract language is blunt for a reason: consumers are told to review the entire contract and all attached statements before signing because the agreement is final and binding unless certain legal obligations were not met. That is not just a technical warning. It is a reminder that a long sales process can leave people vulnerable to rushing the most consequential part. The tactic, intentional or not, is exhausting because it aligns the heaviest legal moment with the lowest mental energy. By the time the customer reaches the fine print, the desire to finish can overwhelm the discipline to slow down.

Key Disclosures That Show Up Late or Too Vaguely

Used-vehicle disclosures are supposed to give buyers meaningful information about what they are purchasing, but a disclosure that appears too late or in overly vague terms still leaves the consumer disadvantaged. A salesperson might mention that a vehicle “had an incident,” “was repaired,” or “was previously commercial” without providing the full context early enough for the shopper to evaluate it properly. The buyer hears enough to feel the issue has been addressed, yet not enough to measure how the fact affects value, risk, or future resale. In practice, incomplete clarity can function a lot like non-disclosure.

Ontario’s rules are extensive because the history of a vehicle can materially alter its worth. OMVIC says dealers must provide written disclosures about past use, history, and condition, and its guidance stresses that accident repairs over $3,000, branding, structural damage, and certain prior uses must be disclosed. The exhaustion comes from the timing and texture of the information. Buyers often do not need more words; they need sharper ones sooner. When material facts are dribbled out after attachment to the vehicle has already formed, the consumer is forced into a difficult emotional recalculation instead of being able to judge the car cleanly from the start.

Accident History Softened Into Something Easier to Swallow

Among the most common frustrations in used-car shopping is the sense that damage history was technically acknowledged but emotionally minimized. A vehicle with significant past repairs may be described in language designed to sound routine: “cosmetic work,” “a minor claim,” “professionally repaired,” or “nothing to worry about.” The issue is not that repaired vehicles should never be sold. Many are repaired properly and honestly. The problem is that shoppers are often asked to react to the tone before they receive the scale. A soft verbal description can lower suspicion long enough for momentum to carry the sale forward.

That matters because written disclosure requirements exist precisely to prevent ambiguity from doing too much work. OMVIC’s guideline states that accident repairs over $3,000 must be disclosed in writing on the bill of sale, and it recommends disclosing as much relevant information as possible because transparency builds trust. Once a buyer has already invested time and emotion, however, even a proper written disclosure can arrive after the main persuasion has happened. The tactic is exhausting because it asks shoppers to reverse a positive impression under pressure. Instead of evaluating the vehicle from neutral ground, they must suddenly reassess whether the history changes everything.

Leaving Lien, Recall, and Title Trouble for the Buyer to Discover

A modern used-car buyer often has to do investigative work that feels wildly out of proportion to the purchase. Beyond mileage and appearance, there are liens, recall records, branding, prior fleet or rental use, province-to-province movement, and, in rare but serious cases, title washing. Regulators and industry resources repeatedly direct buyers to history tools because these issues do not always reveal themselves at first glance. The exhausting part is not merely that such risks exist; it is that the burden of confirming them often falls heavily on the consumer at the exact moment the sales process is urging speed and confidence.

Ontario’s consumer guidance points buyers toward CARFAX, Transport Canada recall information, and the Used Vehicle Information Package for exactly this reason. Recent reporting citing CARFAX Canada data also noted that a large share of checked vehicles carried outstanding debt, creating the risk that an unsuspecting buyer could face repossession issues or cleanup costs later. This tactic, or failure, drains shoppers because it turns a purchase into a verification project. Instead of deciding whether the car is right, the buyer first has to determine whether the car’s paper trail is telling the whole truth.

Ads That Change Meaning Depending on Who Posted Them

Some vehicle ads frustrate shoppers not because the number is false in the usual sense, but because the rules around the ad itself are more complicated than most consumers realize. In Ontario, dealer advertising is subject to all-in pricing rules, but manufacturer advertising is not regulated by OMVIC in the same way. That creates room for a familiar kind of showroom disappointment: a shopper arrives expecting one pricing logic, only to find that the number seen online or in promotional material does not map neatly onto what the dealership is actually prepared to sell for at that moment.

This distinction may sound technical, but for buyers it feels very practical. The average consumer does not approach a car ad with a regulator’s framework in mind. They see a price and assume it is the relevant starting point. OMVIC explicitly notes that manufacturer ads are an exception to the all-in pricing regime it enforces, which helps explain why some price conversations begin with instant friction. The exhaustion comes from having to decode the architecture of the advertisement before even reaching the normal negotiation. Instead of clarifying the market, the ad can become one more layer of uncertainty in a process already full of it.

A Process That Relies on Fatigue as Much as Persuasion

Not every dealership problem is a hidden fee. Sometimes the tactic is simply the structure of the day. The shopper is handed off from salesperson to manager to finance office, waits for figures to be “worked,” revisits terms that seemed settled, and is asked for just one more signature or one more decision. By the end, resistance falls not because every issue has been resolved, but because the buyer wants the experience to be over. Recent Canadian research on used-car shopping has captured this mood directly, with many respondents citing price negotiations, undisclosed issues, and salesperson pressure among the most common frustrations.

That broader pattern matters because it helps explain why even lawful tactics can feel punishing when stacked together. A buyer may face only modest pricing ambiguity, only moderate upsell pressure, only some trade-in fuzziness, and only a little contractual rush. Combined over several hours, the process becomes an endurance contest. The most troubling possibility is that fatigue is not just a side effect but part of the advantage. A worn-down customer is easier to close, easier to upsell, and less likely to restart the search. That may be the clearest reason car shopping so often feels exhausting: the process can reward persistence by the seller more than clarity for the buyer.

22 Things Canadians Do to Their Cars in Spring That Mechanics Hate

Spring brings relief to many Canadian drivers after months of snow, freezing temperatures, and icy roads that put serious strain on vehicles. As temperatures rise across the country, drivers begin washing cars, switching tires, and preparing vehicles for warmer weather and upcoming road trips. However, mechanics across Canada notice the same mistakes every spring when drivers attempt to recover from winter damage. Road salt, potholes, and harsh winter driving conditions often leave vehicles with hidden problems that drivers ignore. Some spring habits even create new mechanical issues that could have been avoided with proper maintenance. Here are 22 things Canadians do to their cars in spring that mechanics hate.

{kind=link}